How are spot commodities priced, and how is my overnight funding calculated?

If you hold a long ‘spot’ position on a commodity with us, it’s important to understand how our markets are priced.

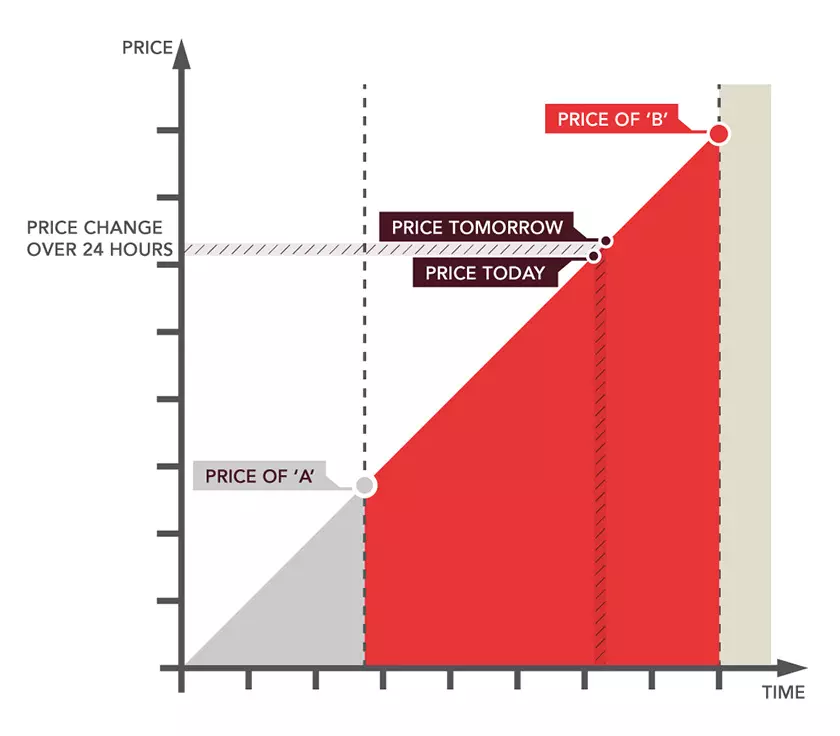

Our spot commodity prices are based on the two nearest futures contracts on the underlying commodity, as these tend to be the most liquid contracts. Over the period we’re pricing from two specific contracts, our spot price gradually moves from the nearest contract to the next.

The ‘front month contract’, the one with the closest expiry date, is labelled ‘A’ in our diagram. The one with the second-nearest expiry date is called the ‘back month contract’ and is labelled ‘B’.

In between these two expiry points, our price gradually moves from the price of ‘A’ towards the price of ‘B’. The price of ‘B’ can be higher or lower than the price of ‘A’.

As with all of our spot markets, you'll pay to hold your position overnight. Due to how our spot commodities are priced, we apply an overnight adjustment – split into two aspects. The first of these is a nightly basis adjustment, which reflects a day’s movement of our spot price from the earlier future contract to the later one. The second is our 3% annual admin fee.

The difference in price between two contracts is dependent on the commodity and market conditions, and can vary substantially. When the difference between these underlying futures prices is amplified, the number of points our market would move on a daily basis also increases. As such, we increase the adjustment.

It is important to note that the increase only relates to the adjustment. This is a response to market conditions, similar to a dividend adjustment on an index, rather than a charge. The only aspect of the adjustment which is a charge is our admin fee, which remains at 3% for standard CFD contracts regardless of market conditions.

You can see a worked example of the basis adjustment and overnight funding for CFDs here.

CFD example

CFD example

The equation for calculating the overnight adjustment is broken down into two parts; the daily movement along the futures curve (basis), and the IG charge. This is applied to positions open at 10pm UK time.

Overnight adjustment = number of contracts x contract size x (basis + IG charge)

Formula for the IG charge = price x 2.5% / 365

Formula for basis = (P3 – P2) / (T2 – T1)

T1 = expiry date of the previous front future

T2 = expiry date of the front future

P2 = price of front future

P3 = price of next future

The basis equates to the daily movement of our undated price along the futures and may be a credit or a debit. This will either be a positive or negative number depending on the direction of your trade and the slope of the forward curve.

For example imagine you are long one $10 contract on US Oil. If there was a time difference between T1 and T2 of 31 days, and front month future (P2) was 4700 and the next future (P3) was 4770 then the overnight adjustment would be calculated as follows:

Overnight adjustment = 1 x $10 x (((4770 – 4700 )/ 31) + (4700 x 2.5% / 365))

= $22.58 + $3.22

In our example the cost to hold the position overnight is $3.22, however you will also see a cash neutral futures curve adjustment as well. The $22.58 basis adjustment will be offset in the running profit or loss on the position.

On the other hand, if you were short US Oil in the above example then you would receive $22.58 and pay $3.22, therefore a net credit of $19.36.

For any position opened before 10pm Friday (UK time) that is still open after 10pm Friday (UK time), the basis adjustment will be made for three days as opposed to one. This three-day adjustment is applied on the Sunday night or Monday morning.