If you hold a long ‘spot’ position on a commodity with us, it’s important to understand how our markets are priced.

Our spot commodity prices are based on the two nearest futures contracts on the underlying commodity, as these tend to be the most liquid contracts. Over the period we’re pricing from two specific contracts, our spot price gradually moves from the nearest contract to the next.

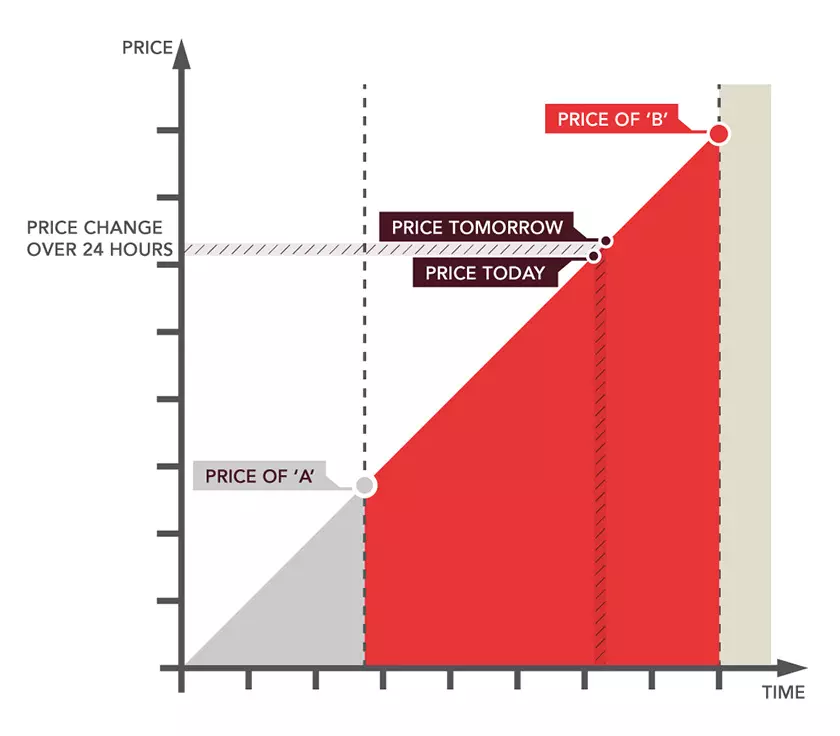

The ‘front month contract’, the one with the closest expiry date, is labelled ‘A’ in our diagram. The one with the second-nearest expiry date is called the ‘back month contract’ and is labelled ‘B’.

In between these two expiry points, our price gradually moves from the price of ‘A’ towards the price of ‘B’. The price of ‘B’ can be higher or lower than the price of ‘A’.

As with all of our spot markets, you'll pay to hold your position overnight. Due to how our spot commodities are priced, we apply an overnight adjustment – split into two aspects. The first of these is a nightly basis adjustment, which reflects a day’s movement of our spot price from the earlier future contract to the later one. The second is our 2.5% annual admin fee.

The difference in price between two contracts is dependent on the commodity and market conditions, and can vary substantially. When the difference between these underlying futures prices is amplified, the number of points our market would move on a daily basis also increases. As such, we increase the adjustment.

It is important to note that the increase only relates to the adjustment. This is a response to market conditions, similar to a dividend adjustment on an index, rather than a charge. The only aspect of the adjustment which is a charge is our admin fee, which remains at 2.5% for spread bets and standard CFD contracts regardless of market conditions.

You can see a worked example of the basis adjustment and overnight funding for spread betting and CFDs here.

Spread bet example

Spread bet example

The equation for calculating the overnight adjustment is broken down into two parts; the daily movement along the futures curve (basis), and the IG charge. This is applied to positions open at 10pm UK time.

Overnight adjustment = amount/pt x (basis + IG charge)

Formula for the IG charge = Price x 2.5% / 365

Formula for basis = (P3 – P2) / (T2 – T1)

T1 = expiry date of the previous front future

T2 = expiry date of the front future

P2 = price of front future

P3 = price of next future

The basis equates to the daily movement of our undated price along the futures and may be a credit or a debit. This will either be a positive or negative number depending on the direction of your trade and the slope of the forward curve.

For example, imagine you are long £10/pt on US Oil. If there was a time difference between T1 and T2 of 31 days, and front month future (P2) was 4700 and the next future (P3) was 4770 then the overnight adjustment would be calculated as follows:

Overnight adjustment = £10 x ((4770 – 4700 / 31) + (4700 x 2.5% / 365))

= £22.58 + £3.22

In our example the cost to hold the position overnight is £3.22, however you will also see a cash neutral futures curve adjustment as well. The £22.58 basis adjustment will be offset in the running profit or loss on the position.

On the other hand, if you were short US Oil in the above example then you would receive £22.58 and pay £3.22, therefore a net credit of £19.36.

For any position opened before 10pm Friday that is still open after 10pm Friday, the basis adjustment will be made for three days as opposed to one. This three-day adjustment is applied on the Sunday night or Monday morning.

CFD example

CFD example

The equation for calculating the overnight adjustment is broken down into two parts; the daily movement along the futures curve (basis), and the IG charge. This is applied to positions open at 10pm UK time.

Overnight adjustment = number of contracts x contract size x (basis + IG charge)

Formula for the IG charge = price x 2.5% / 365

Formula for basis = (P3 – P2) / (T2 – T1)

T1 = expiry date of the previous front future

T2 = expiry date of the front future

P2 = price of front future

P3 = price of next future

The basis equates to the daily movement of our undated price along the futures and may be a credit or a debit. This will either be a positive or negative number depending on the direction of your trade and the slope of the forward curve.

For example imagine you are long one $10 contract on US Oil. If there was a time difference between T1 and T2 of 31 days, and front month future (P2) was 4700 and the next future (P3) was 4770 then the overnight adjustment would be calculated as follows:

Overnight adjustment = 1 x $10 x ((4770 – 4700 / 31) + (4700 x 2.5% / 365))

= $22.58 + $3.22

In our example the cost to hold the position overnight is $3.22, however you will also see a cash neutral futures curve adjustment as well. The $22.58 basis adjustment will be offset in the running profit or loss on the position.

On the other hand, if you were short US Oil in the above example then you would receive $22.58 and pay $3.22, therefore a net credit of $19.36.

For any position opened before 10pm Friday that is still open after 10pm Friday, the basis adjustment will be made for three days as opposed to one. This three-day adjustment is applied on the Sunday night or Monday morning.

Related questions

Improve your skills

Become a better trader with IG Academy. Take engaging step-by-step courses, attend expert-led seminars and webinars.

Get peer support

Have your questions answered by like-minded traders and IG staff over at IG Community.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money. Clients can lose more than they deposit. All trading involves risk.

IG is a trading name of IG Markets Limited and IG Markets South Africa Limited. IG Markets South Africa Limited offers domestic accounts and IG Markets Limited offers international accounts.

IG Markets South Africa Limited is authorised and regulated by the Financial Sector Conduct Authority (in South Africa) as an over-the-counter derivative provider and an authorised financial services provider (FSP No 41393). IG Markets Limited is authorised and regulated by the Financial Conduct Authority (in the UK).

IG provides execution only services and enters into principal-to-principal transactions with its clients on IG’s prices. Such trades are not on exchange. Whilst IG Markets South Africa Limited is a regulated FSP and acts as an intermediary as understood in the FAIS Act in relation to the international accounts offered by IG Markets Limited, CFDs issued by IG are not regulated by the FAIS Act as they are undertaken on a principal-to-principal basis. CFDs issued by IG Markets South Africa Limited are regulated by the Financial Markets Act, and IG Markets South Africa Limited is a licenced over-the-counter derivative provider.

South African residents are required to obtain the necessary tax clearance certificates in order to utilise their foreign investment allowance should the South African resident wish to open an international account with IG Markets Limited.

The information on this site is not directed at residents of the United States or Belgium or any particular country outside South Africa and is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

Voted SA’s top CFD provider in Business Day Investors Monthly Annual Stockbroker Awards in 2012, best platform for Active Day Traders in 2013 and 2014, SA's best Online Broker in 2015 and 2017 and SA's best CFD provider in 2020 as well as SA's Top CFD Broker in 2021.

© 2003 - 2023