Hang Seng 2024 outlook

It has been quite an unexpectedly turbulent year for the Hang Seng index, which is on track to mark its fourth consecutive year of decline, a stark contrast to other global markets.

It has been quite an unexpectedly turbulent year for the Hang Seng index, which is on track to mark its fourth consecutive year of decline, a stark contrast to other global markets.

Hang Seng 2023 review

China’s exit from its Covid-zero restriction in the final month of 2022 led many to believe that 2023 would be a year of recovery for the beleaguered Chinese and Hong Kong investment markets. Thus, the optimism following China's reopening initiated a positive uptrend for Hong Kong stocks in the first month of 2023. However, it turned out that the beginning of the year was also its peak.

Since then, worrying signs started emerging across all corners of the Chinese economy, from a sharp downturn in the property sector, deflationary domestic consumption to a slumping export market. All these factors snowballed into a widespread systemic and confidence crisis for the world’s second largest economy and its investment markets. Consequently, the Hang Seng index had fallen more than 20% and entered bear market territory in August and reached its yearly low in December.

Jan

|

Feb |

March |

Apr |

May |

June |

July |

Aug |

Sep |

Oct |

Nov |

|

Monthly%

|

+10.4% |

-9.4% |

+3.1% |

-2.5% |

-8.3% |

+3.7% |

+6.1% |

-8.5% |

-3.1% |

-3.9% |

-0.6% |

Source: Hang Seng Index

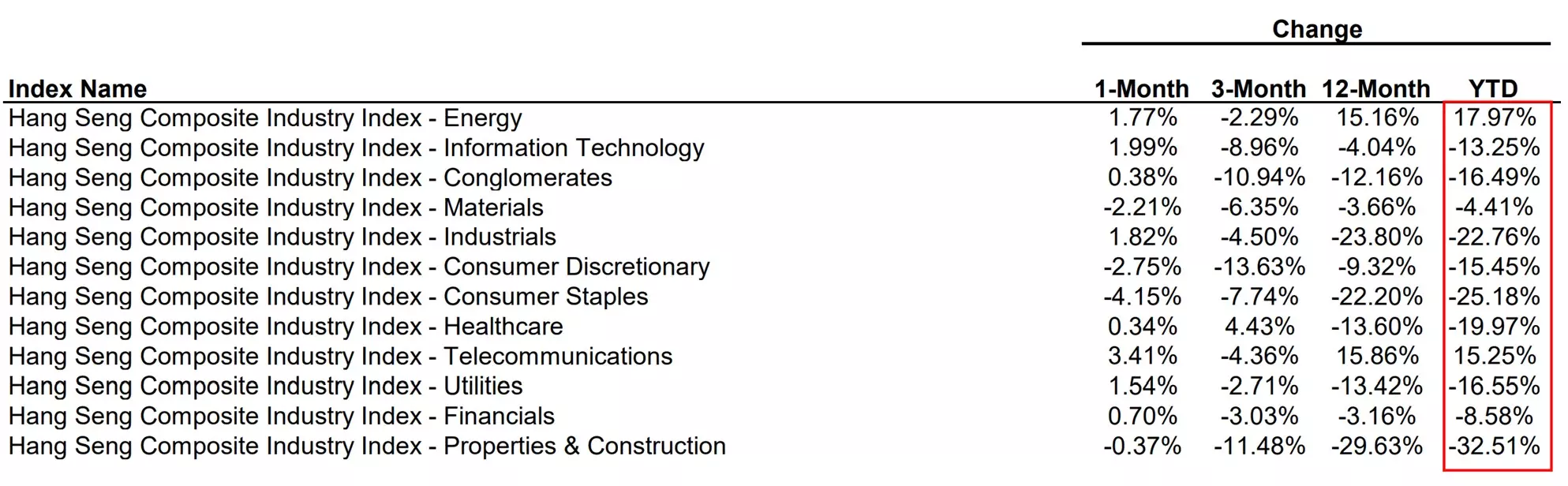

In terms of each sector’s performance, as of the end of November, the energy and telecommunications sectors were the only two to register gains, rising by 17.97% and 15.25%, respectively. In contrast, the property and consumer sectors endured significant losses, by more than 20%, primarily attributed to the intensified property crisis in mainland China and a contracting domestic consumption market.

Hang Seng 2024 outlook

Looking ahead, it’s likely that the Hang Seng Index may continue to grapple with the repercussions of years of decline and underperformance in the upcoming year. The index has been left far behind with an average 11% loss in the past four years while its peer markets like US and Japanese stocks moving substantially higher. The gap, unfortunately, may continue to widen as the fleet of global capital liquidity due to the lack of confidence for a speedy recovery. In October 2023, Hang Seng’s trading volume was down 20% year over year following a 10% down in the previous month.

In October 2023, the Hang Seng's trading volume declined by 20% year over year, following a 10% decrease in the previous month. This further underscores the challenges and uncertainties faced by the index and the prevailing cautious sentiment among investors.

Hang Seng index/US stocks/Japan stocks five-year performances

Additionally, despite China’s GDP is expected to grow by 5.4% this year (2023) according to IMF, there’s a prevailing expectation that a much slower economic growth will become the “new norm” for China. The continued weakness in the property sector, together with subdued internal and external demand could restrict the growth of Chinese economy to fall below 5%, the lowest level in over two decades.

If there's any reason for optimism, one of the main sources to look forward to could be the large-scaled fiscal stimulus support from Beijing. Since the second quarter of 2023, the Chinese government has explored various ways to reinvigorate the investment market, including the issuance of an additional $137 billion in sovereign debt and a rare mid-year increase in the fiscal deficit. While the impacts of these measures seemed to be mostly short-lived in the stock market, these top-down supports could potentially lay the groundwork for a rebound in economic activities in the year to come.

Furthermore, following a year of disappointment, it's also possible that global investors' lofty expectations will be adjusted, thereby lowering the bar for Hong Kong stocks to shine.

Hang Seng Index technical analysis

From a technical perspective, the Hang Seng index appears to be following a downward trajectory since the peak in January and is on track to revisit the floor level since 2009. However, over the short term, the downtrend may stabilize near the crucial psychological level at 16000 with the oversold signals suggesting a rebound could be in sight.

On the upside, a renewed push higher above 17,800 could pave the way to challenge the November high, with the potential to reach the 20-week moving average (MA) above 17,900.

Hang Seng Index weekly chart

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Take a position on indices

Deal on the world’s major stock indices today.

- Trade the lowest Wall Street spreads on the market

- 1-point spread on the FTSE 100 and Germany 40

- The only provider to offer 24-hour pricing

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.