ASX200 Mid Year Review 2023

As we approach the halfway mark of 2023, the ASX200 is up a tepid 2.24% for the Calendar Year to Date (CYTD).

A return well below what might have been expected after the ASX200 leapt from the starting blocks in January (+6.22%) on optimism around the China reopening and hopes that the headwinds of rising interest rates and inflation encountered in 2022 were in the rear vision mirror.

Unfortunately, that optimism has proved to be somewhat misplaced. Confounding most, the reopening in China has disappointed to the point that Chinese authorities recently responded by easing policy to prevent a double-dip slowdown.

While a lack of growth/technology stocks within the index cushioned the ASX200 from the bear market that the Nasdaq encountered in 2022, the same lack of technology stocks meant the ASX200 has not benefitted from the Nasdaq’s spectacular rebound in 2023.

However, the ASX200 has not only been left in the shadows by indices with a high concentration of tech stocks.

Global peers, including the Japanese stock market, the Nikkei, is up 27.2% CYTD, the German stock market, the DAX, is up 17% CYTD, and the benchmark US stock index, the S&P500, is up 14.63%. Most closely mirroring the ASX200s returns, the Dow Jones is up just 2.35%.

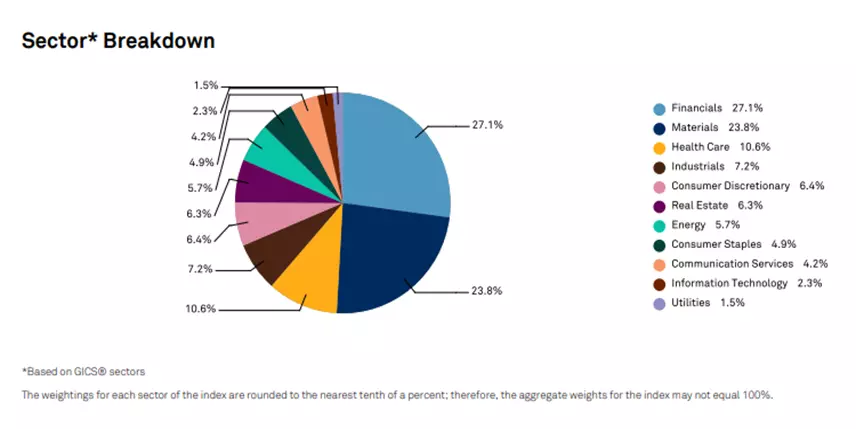

ASX200 Sector Analysis

Drilling down by sector, a clearer picture starts to emerge. The IT (+26.80%), Telecom (+8.59%), and Industrial (+8.83%) sectors have been the strongest-performing ASX200 sectors in 2023. However, these three sectors combined account for a paltry ~13.5% of the index.

In contrast, the largest sector, the Financial Sector, which accounts for 27.1% of the index, is down 2.79% CYTD. The third largest sector, Health Care, which accounts for 10.06% of the index, is up just 0.02% on the year. The second largest sector, Materials, which accounts for a punchy 23.8% of the index, is up just 3.34% CYTD.

The Financial Sector has become the Achilles heel for the ASX200 in 2023. Rising interest rates have bought stress to the global banking system. Locally banks are experiencing Net Interest Margin (NIM) compression into a slowing economy, which has raised expectations that bank earnings have peaked and downgrades may follow.

Elsewhere, China’s slower-than-expected economic recovery during the first half of 2023 has weighed on the commodity prices, providing another headwind via the local bourse’s heavy exposure to resource stocks.

Macro Analysis

The negatives

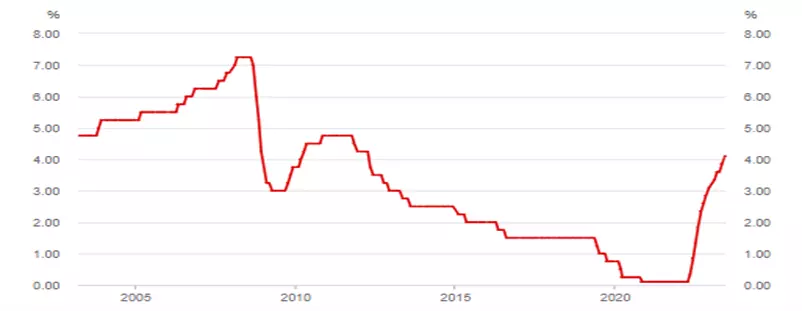

Reserve Bank of Australia (RBA) – The key local macro event in 2023 has been a continuation of the RBA’s rate hiking cycle, which many expected to end late last year. In recent months the RBA appears to have lost patience with persistently high inflation, and following back-to-back “surprise” 25 basis point (bp) rate hikes, the interest rate market expects an RBA peak rate of 4.6% before year-end.

GDP (Gross Domestic Product) – quarter one (Q1) 2023 GDP rose by 0.2% QoQ (quarter on quarter) for an annual rate of 2.3%. While this was the sixth consecutive period of economic growth, it was the slowest rate since major covid-19 pandemic restrictions ended. The subdued GDP reading shows that rising interest rates and cost of living pressures are slowing the economy. The household saving rate fell to 3.7%, its lowest level since 2008.

Inflation – In May, the Monthly headline consumer price index (CPI) indicator eased to 5.6% year-over-year (YoY) from 6.8% in April. The trimmed mean (core inflation) eased to 6.1%YoY from 6.7% in April. Both measures remain well above the RBAs target band of 2-3%.

Summary – Elevated inflation, rising interest rates and slowing growth are headwinds for equities and the ASX200.

The Positives

China – Chinese authorities recently cut key lending rates following a run of soft Chinese growth and activity data. The rate cuts are expected to be part of a broad package of stimulus measures. The shift towards easier policy in China is a tailwind for ASX-listed resource stocks and the ASX200.

Technical Analysis

The ASX200 has spent the past three months trading sideways in a range between resistance at 7370/7390 and support at 7075/7055.

Until the ASX200 sees a sustained break of either of these levels, further sideways-range trading is expected. Aware that a sustained break of range extremes should see the ASX200 extend the move by 150 points (~2%) in the direction of the break.

Summary

Balancing out the headwinds of elevated inflation, higher interest rates, and slowing growth against the tailwinds of expected China stimulus, we look for the ASX200 to finish the year at 7350.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Take a position on indices

Deal on the world’s major stock indices today.

- Trade the lowest Wall Street spreads on the market

- 1-point spread on the FTSE 100 and Germany 40

- The only provider to offer 24-hour pricing

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.