Rand price weaker after local inflation data and ahead of SARB rates decision

There is, however, still a slight chance that the SARB will raise rates by another 25 basis points, although this is not our base case.

When is the SARB MPC rates decision?

South African Reserve Bank (SARB) concludes its Monetary Policy Committee (MPC) meeting on Thursday the 23rd of November 2023 and is scheduled to announce changes (if any) to local lending rates at around 3pm. This marks the last SARB MPC meeting for 2023.

How much will the SARB raise rates by at the MPC meeting?

Consensus estimates suggest that the SARB will keep lending rates on hold at the upcoming meeting, leaving the repurchase (repo) rate at 8.25% and the prime lending rate at 11.75%.

Some of the mitigating factors which have seen consensus expectations move from a 25-basis point hike to a hold scenario, include a stronger rand and lower fuel prices, strength in the ZAR and the suggestion that the US will keep lending rates on hold as well at its final Federal Reserve meeting for the year.

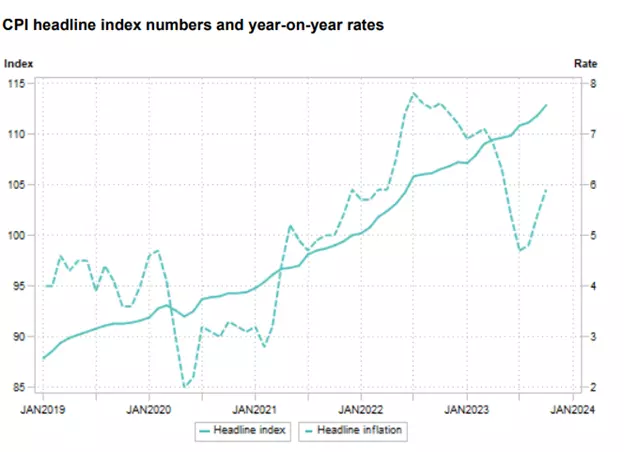

October CPI Inflation

Annual consumer price inflation rose to 5.9% in October 2023, a significant increase from 5.4% in September 2023. The Consumer Price Index (CPI) witnessed a month-on-month increase of 0.9% in October 2023.

The key contributors to the 5.9% annual inflation rate were:

- Food and non-alcoholic beverages, which increased by 8.7% year-on-year and contributed 1.6 percentage points.

- Housing and utilities, which saw a year-on-year increase of 5.4%, contributing 1.3 percentage points.

- Transport, which surged by 7.4% year-on-year, contributing 1.1 percentage points.

- Miscellaneous goods and services, which increased by 5.3% year-on-year, contributing 0.8 percentage points.

In October, the annual inflation rate of goods was 8.1%, up from 6.8% in September. However, the rate for services was 3.8%, slightly down from 4.0% in September.

The above graph highlights the uptrend in the headline CPI index (left axis) and annualized inflation rate (right axis).

Food and transport (fuel) have once again led the local CPI inflation higher, reaching a figure of 5.9% y/y. This is worse than consensus estimates had predicted, yet still marginally below the South African Reserve Bank's (SARB) targeted 6% ceiling.

The higher-than-expected inflation figure may create some apprehension for tomorrow’s interest rate decision by the SARB. However, with fuel prices in November being substantially lower and the rand trading well off its worst levels, this might aid the Quarterly Projection Model and see rates maintained at current levels.

There is, however, still a slight chance that the SARB will raise by another 25 basis points, although this is not our base case. The Federal Reserve is unlikely to raise rates again this year, and global policy appears to be at the top of the cycle. It's likely that the SARB will follow suit as well.

USD/ZAR

Following the bullish price reversal off the 18.10 level and break above the 18.40 level, the USD/ZAR has rallied to and is now testing resistance at 18.70.

The short-term momentum is up for the currency pair. A close above 18.70 would suggest 18.85 as a further upside target from the move. A close above 18.85 could unlock further gains towards the next level of resistance considered at 19.35. Traders who are long might consider trailing their respective stops to a close below the one day low.

This information has been prepared by IG, a trading name of IG Markets Ltd and IG Markets South Africa Limited. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients. See full non-independent research disclaimer and quarterly summary.

Live prices on most popular markets

- Forex

- Shares

- Indices

Prices above are subject to our website terms and agreements. Prices are indicative only