Key events to watch in the week ahead: 15 - 21 April 2024

What are some of the key events to watch next week?

This week’s overview

It was a mixed week for Wall Street, as a higher-than-expected US inflation read for the third straight month called for markets to readjust their Federal Reserve (Fed) rate expectations once more. Market participants are now pricing out a rate cut in June and pushing back the rate-cut timeline to September instead. The scale of rate cuts this year is also revised down to two cuts, versus the original three being priced before the consumer price index (CPI) release.

Ahead, the upcoming US earnings season may aid to draw some attention away from Fed’s policy outlook. The recent run in stronger-than-expected US economic data seems likely to fuel more soft-landing talks, while paving the way for earnings recovery momentum to continue.

Into the new week, here are five things on our radar.

US earnings season: Goldman Sachs, Johnson & Johnson, Bank of America, Morgan Stanley, Netflix

The US earnings season will resume next week with results from major US banks, notably from Goldman Sachs, Bank of America and Morgan Stanley (24 Hours). Thus far, expectations are for the broad earnings recovery trend to continue, with 1Q earnings for the S&P 500 expected to grow 3.2% year-on-year (YoY), which will mark the third-straight quarter of earnings growth. Netflix will also be the highlight, with market participants watching if its stellar subscriber growth in the previous earnings release can be mirrored into the 1Q results as well.

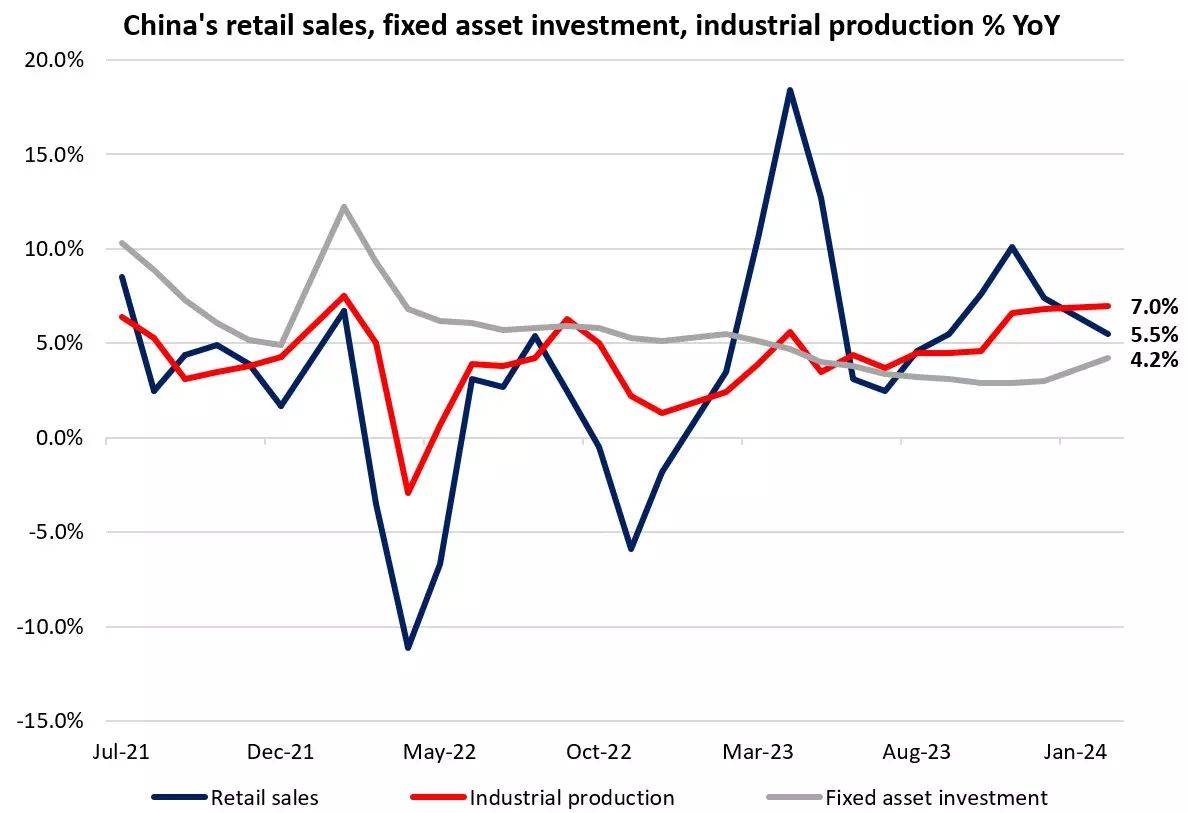

16 April 2024 (Tuesday, 10am SGT): China’s 1Q GDP, industrial production, retail sales and fixed asset investment

The recent run in China’s economic data continues to highlight a mixed picture for the country’s economic recovery. While upside surprises in its March Purchasing Managers' Index (PMI) numbers offered room for some relief, market participants will have to balance it with unresolved risks in the property sector, alongside prevailing weakness in domestic demand.

Price data for March showed China’s consumer prices flirting with deflationary territory once more, coming in lower-than-expected at just 0.1% year-on-year, down from the previous 0.7% in February.

Economic data releases next week may reflect more of the same in terms of easing recovery momentum. March industrial production is expected to ease to 5.4% YoY from previous 7.0%, while retail sales is expected to ease to 4.5% YoY from previous 5.5%. Expectations are for 1Q gross domestic product (GDP) to register a 4.6% growth, lower than the 5.5% in 4Q 2023. Quarter-on-quarter, 1Q GDP is expected to come in at 1.4% from previous 1.0%.

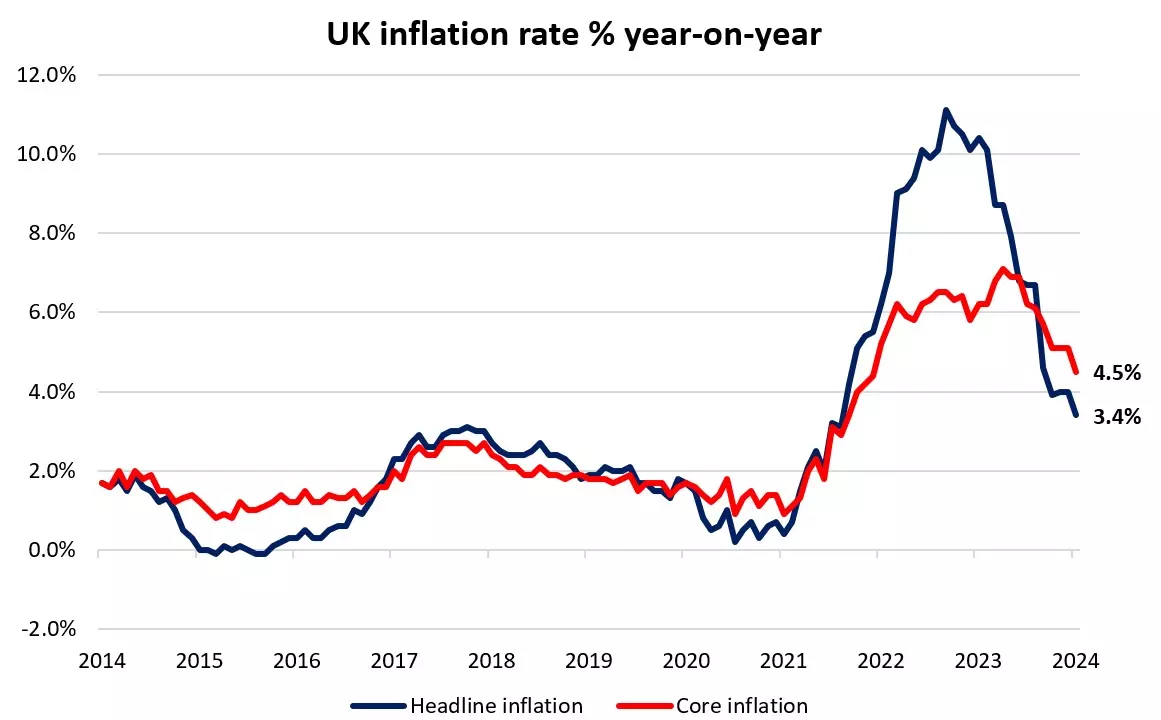

17 April 2024 (Wednesday, 2pm SGT): UK’s inflation rate

In February, UK headline inflation rate eased to 3.4% YoY from 4.0% in January, below market expectations of 3.5%. It was the lowest rate since September 2021. The annual core inflation rate fell to 4.5% from 5.1% prior, below market expectations of 4.6%.

The softer inflation data fell the day before the Bank of England (BoE)’s March Board meeting when the BoE shifted to a neutral stance, viewed as the first step towards rate cuts. The BoE said it will “continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation".

The initial response in the rates market was to price a cumulative 75 basis point (bp) of BoE rate cuts this year. However, following the hotter-than-expected US CPI data this week, the rates market is pricing in just 50 bp of cuts, with a first-rate cut priced in September.

This month (March), the annual rate of headline inflation is expected to fall to 3.1% from 3.4%, and the annual rate of core inflation is expected to ease to 4.3% from 4.5%.

18 April 2024 (Thursday, 9.30am SGT): Australia’s employment change

Last month (February), the Australian economy added 116.5k jobs, versus consensus expectations of +40k. The robust increase in jobs saw the unemployment rate fall to 3.7%, the lowest since September 2023, from 4.1% prior. The participation rate ticked up to 66.7% from 66.6%. Meanwhile, the underutilisation rate, which combines the unemployment and underemployment rates, fell by 0.5 percentage points to 10.3%.

The Australian Bureau of Statistics (ABS) noted that the solid job growth in February followed a “larger than usual number of people in December and January who had jobs that they were waiting to start or to return to. This translated into a larger-than-usual flow of people into employment in February, even more so than in February last year.”

This month (March), the market expects the economy to lose 70k jobs and the unemployment rate to rebound to 4% from 3.7%. With seasonal noise expected to subside in the coming months, allowing evidence of cooling within the labour market to emerge more clearly, we reiterate our call for the Reserve Bank of Australia (RBA) to cut rates by 25 bp in August before a second cut in November, which will see the cash rate end the year at 3.85%.

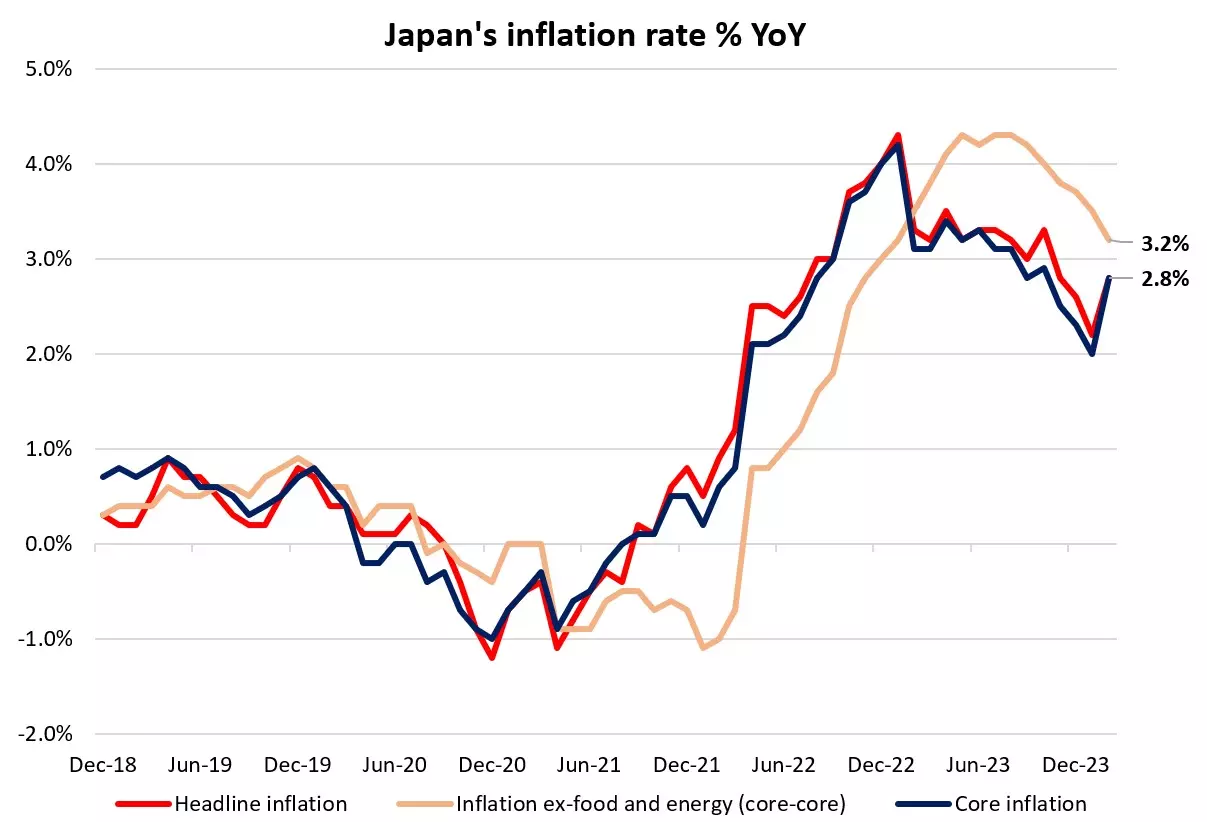

19 April 2024 (Friday, 7.30am SGT): Japan’s inflation rate

Both Japan’s headline and core inflation rate accelerated in February to 2.8% YoY, but its core-core inflation (which excludes fresh food and energy) continues to ease to 3.2% from previous 3.5%. The core-core aspect is closely watched by the Bank of Japan (BoJ) as an indicator of broader price trends, and a touch of its lowest level since January 2023 injects some uncertainty on the BoJ’s next move.

In the previous BoJ meeting, the central bank raised its short-term interest rates for the first time in 17 years, with the hopes that a wage-price spiral may make its ‘stable and sustainable inflation’ goal more achievable. Recent follow-up comments by the BoJ Governor Kazuo Ueda also guided that the central bank may look to reduce monetary stimulus further if trend inflation rises.

Further clues on the timing of the BoJ’s next rate hike will be sought from the upcoming inflation data, with any upward pressures on prices likely to see its inflation forecasts raised at the upcoming April meeting. That may drive some hawkish rate expectations, with current consensus priced for the BoJ to hike rates further in July this year.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.