Amortisation definition

What is amortisation?

Amortisation is the process of spreading the repayment of a loan, or the cost of an intangible asset, over a specific timeframe. This is usually a set number of months or years, depending on the conditions set by banks or copyright agencies. Amortisation will often incur interest payments, set at the discretion of the lender.

Amortisation vs depreciation

While amortisation covers intangible assets – such as patents, trademarks and copyrights – depreciation is the method of spreading the cost of a tangible asset. These are physical assets, such as computers, vehicles, machinery and office furniture.

Unlike depreciation, amortisation is often paid in consistent instalments – meaning that the same amount will be repaid each month or year until the debt is paid. With depreciation, borrowers will often repay more at the start of the borrowing period, so that they pay less towards the end. This is because a tangible asset’s inherent value might decrease over the course of its life, which means it will be worth less the older it is, or the more it is in use.

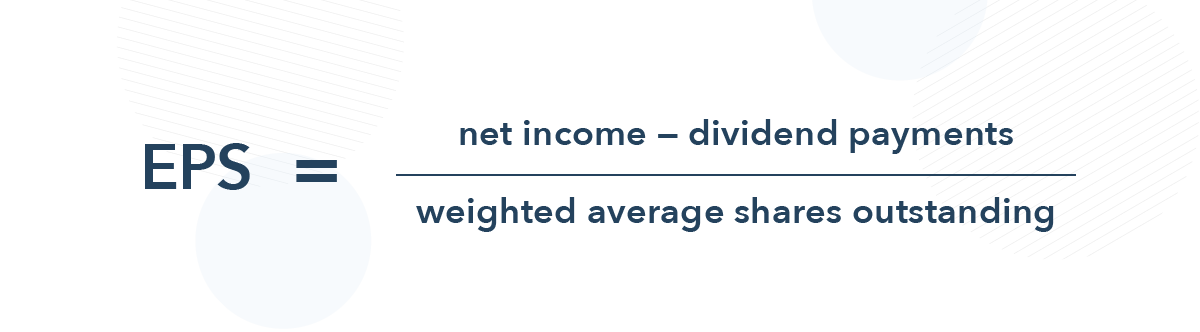

How to calculate amortisation

The formula for calculating the amortisation of a loan is one of the simplest repayment models available. It uses the formula shown below:

Amortisation examples

Let’s suppose that company A has an outstanding debt of $5 million. If that company repaid $250,000 of that loan every year, it would be said that $250,000 of the debt is being amortised each year. However, company A would also need to pay interest on the loan.

In this case, if we suppose that the interest rate is set at 10%, then company A would actually need to repay $275,000 per year for the debt to be fully amortised.

As another example, let’s say that you had been given ten years to repay $1.5 million in business loans to a bank on a monthly basis. In order to work out your monthly amortisation obligations, you would divide $1.5 million by ten, giving you $150,000 per year.

You would then divide this by 12, giving you $12,500 which you would need to repay each month until the debt was fully amortised. Accounting for a 5% interest rate, your final total to be repaid each month would be $13,125.

Build your trading knowledge

Discover how to trade with IG Academy, using our series of interactive courses, webinars and seminars.

Contact us

New client: +65 6390 5133 or accountopening@ig.com.sg

Clients: Help and support

WhatsApp: Click here